Legal Deed in Lieu of Foreclosure Document

Legal Deed in Lieu of Foreclosure Document

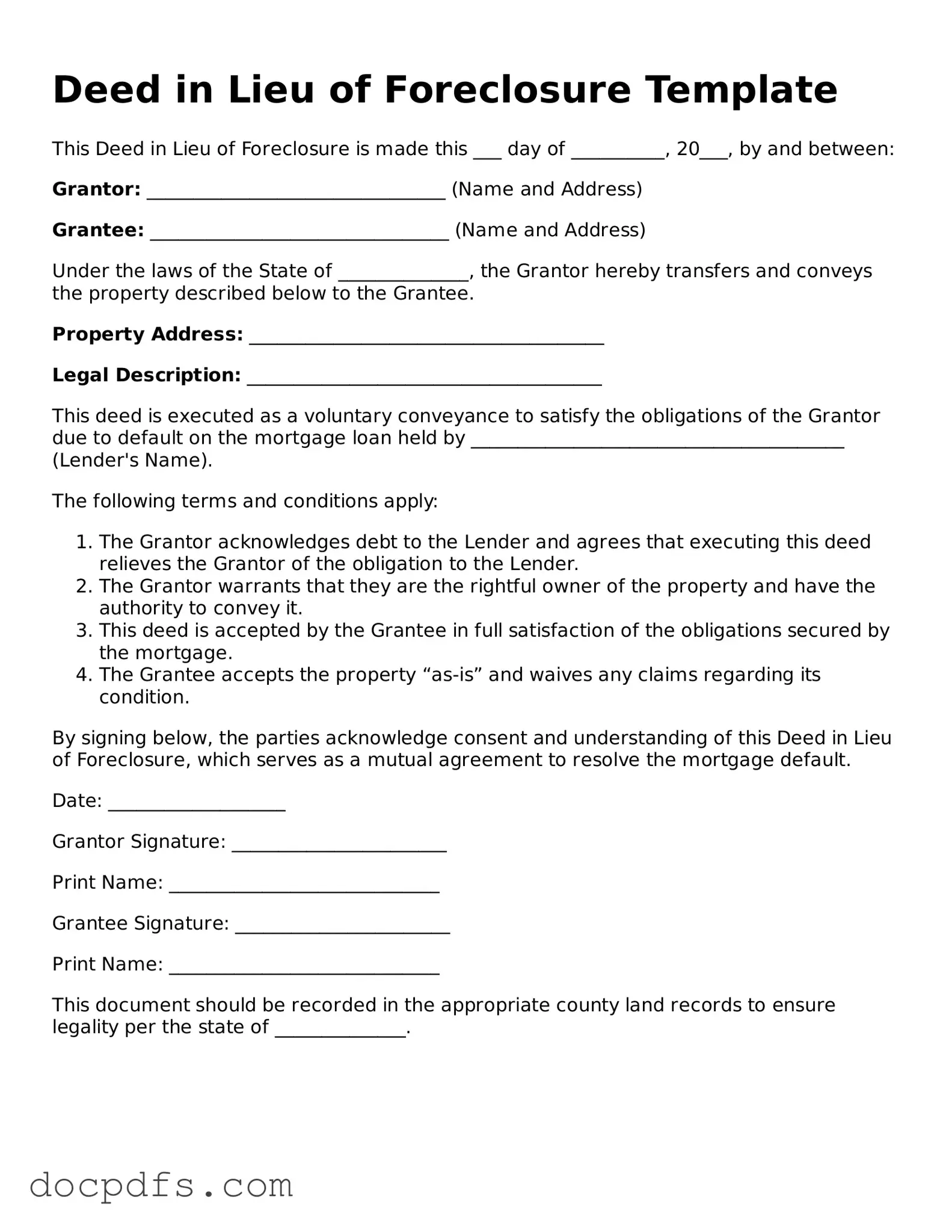

The Deed in Lieu of Foreclosure form serves as a significant legal instrument in the realm of real estate transactions, particularly for homeowners facing financial difficulties. This form enables a property owner to voluntarily transfer ownership of their property to the lender, thereby avoiding the lengthy and often costly foreclosure process. By executing this document, the homeowner relinquishes their rights to the property in exchange for the cancellation of the mortgage debt. This arrangement can provide a more amicable solution for both parties, as it allows the lender to recover the property without the need for court intervention. Additionally, the Deed in Lieu of Foreclosure can help mitigate the negative impact on the homeowner's credit score compared to a formal foreclosure. The process typically involves negotiations between the homeowner and the lender, ensuring that all terms are clearly outlined and understood. It is essential for individuals considering this option to be aware of the implications and requirements associated with the form, as well as any potential tax consequences that may arise from the transfer of property ownership.

Quitclaim Deed Form New Jersey - A quitclaim deed is often used in situations where the parties know each other well and trust one another.

A FedEx Bill of Lading is a crucial document used in the transportation of goods, serving as a receipt for freight services and a contract between the shipper and the carrier. It outlines essential information such as the service type, origin and destination addresses, and any special instructions for handling. To simplify your shipping process, fill out the form by clicking the button below and visit https://pdfdocshub.com/ for additional resources.

Transfer on Death Deed California - Using a Transfer-on-Death Deed can simplify the overall estate settlement process.

A Deed in Lieu of Foreclosure is a legal document that allows a homeowner to transfer ownership of their property to the lender to avoid foreclosure. This process often involves several other forms and documents that facilitate the transaction. Below is a list of common documents that may accompany a Deed in Lieu of Foreclosure.

Each of these documents plays a crucial role in the process of completing a Deed in Lieu of Foreclosure. Understanding their purpose can help homeowners navigate this challenging situation more effectively.

When filling out the Deed in Lieu of Foreclosure form, attention to detail is crucial. Here are nine important do's and don'ts to consider:

When considering a Deed in Lieu of Foreclosure, it's important to understand the implications and processes involved. Here are key takeaways to keep in mind:

Understanding these points can help you make informed decisions regarding your property and financial future.

After completing the Deed in Lieu of Foreclosure form, you will need to submit it to your lender for review. They will assess the document and determine the next steps. It is important to ensure that all information is accurate and complete to avoid delays in the process.

A Deed in Lieu of Foreclosure is a legal document that allows a homeowner to voluntarily transfer their property to the lender to avoid foreclosure. This option can be beneficial for both parties, as it can help the homeowner avoid the negative consequences of foreclosure and allow the lender to take possession of the property more quickly.

Eligibility for a Deed in Lieu of Foreclosure typically includes:

There are several benefits, including:

While there are benefits, there can also be drawbacks, such as:

The process typically involves several steps:

Not necessarily. Depending on the agreement with your lender, you may be allowed to stay in the home for a certain period after the deed is signed. It's important to discuss this with your lender to understand the specific terms.

Once you initiate a Deed in Lieu of Foreclosure, you cannot sell the home. The property will be transferred to the lender, and you will no longer own it. If you are considering selling, it may be best to explore that option first.

A Deed in Lieu of Foreclosure will still have a negative impact on your credit score, but it is generally less severe than a foreclosure. The exact effect will depend on your overall credit profile and the scoring model used by lenders.