Free Florida Promissory Note Form

Free Florida Promissory Note Form

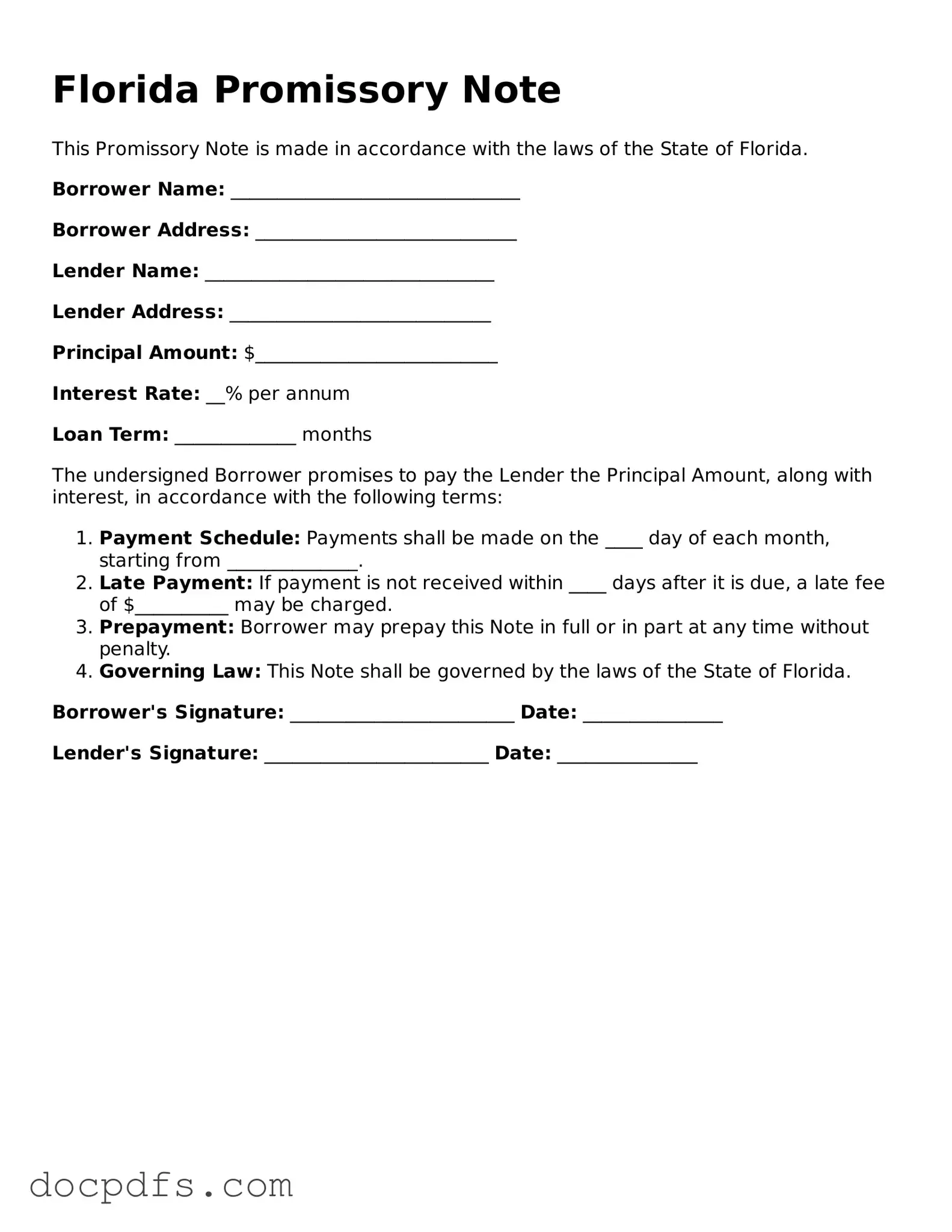

The Florida Promissory Note form serves as a vital document in financial transactions, particularly when one party borrows money from another. This legally binding agreement outlines the borrower's promise to repay the loan amount, specifying the terms of repayment, including interest rates, payment schedules, and the consequences of default. It is essential for both lenders and borrowers to understand the details contained within this form, as it protects the rights of both parties involved. Additionally, the document may include clauses addressing prepayment options, late fees, and the governing law, which is crucial for resolving any disputes that may arise. By clearly delineating the expectations and obligations of each party, the Florida Promissory Note fosters transparency and trust, making it a cornerstone of many financial agreements in the state.

Promissory Note Template Georgia - Can impact the borrower's credit score based on repayment history.

Texas Promissory Note Requirements - The simplicity of a promissory note allows for easy comprehension, making it accessible to a wide range of individuals.

To facilitate the sale process, sellers and buyers should make use of the appropriate documentation, such as the Texas Motor Vehicle Bill of Sale form, which can be accessed at texasformsonline.com/free-motor-vehicle-bill-of-sale-template/. This ensures that all important details regarding the transaction are correctly recorded, aiding both parties in a smooth exchange and proper vehicle registration.

How to Write a Promissory Note Example - The presence of witnesses can sometimes provide additional security for a signed promissory note.

The Florida Promissory Note is a crucial document in lending agreements, outlining the terms under which a borrower agrees to repay a loan. Alongside this form, several other documents are commonly used to ensure that both parties understand their rights and obligations. Below is a list of some of these important forms and documents.

These documents work together to create a clear framework for the lending relationship, ensuring that both parties are aware of their responsibilities and rights. Understanding each document's purpose can help facilitate a smoother transaction and reduce the risk of misunderstandings.

When filling out the Florida Promissory Note form, it’s important to be careful and thorough. Here are some things to keep in mind:

Following these guidelines can help ensure your Promissory Note is completed correctly. If you have any doubts, consider seeking assistance.

Filling out and using a Florida Promissory Note form requires careful attention to detail. Here are some key takeaways to keep in mind:

By following these guidelines, you can ensure that your Florida Promissory Note is clear, comprehensive, and legally binding.

Once you have the Florida Promissory Note form ready, it's time to fill it out accurately. This form is essential for documenting a loan agreement between a borrower and a lender. Make sure to have all necessary information at hand to ensure a smooth process.

A Florida Promissory Note is a written promise to pay a specific amount of money to a designated person or entity at a specified time or on demand. This document outlines the terms of the loan, including the interest rate, payment schedule, and any consequences for defaulting on the loan. It serves as a legal record of the agreement between the borrower and the lender.

Any individual or business in Florida can use a Promissory Note. It is commonly used in various situations, such as personal loans between friends or family, business loans, or real estate transactions. Both the borrower and lender must agree to the terms outlined in the note.

A typical Florida Promissory Note includes the following key components:

Yes, a Florida Promissory Note is legally binding as long as it meets certain requirements. Both parties must sign the document, and it should clearly outline the terms of the loan. If either party fails to comply with the terms, the note can be enforced in a court of law.

While notarization is not legally required for a Florida Promissory Note to be valid, it is highly recommended. Having the document notarized adds an extra layer of authenticity and can help prevent disputes about the validity of the signatures or the agreement.

Yes, a Florida Promissory Note can be modified after it has been signed, but both parties must agree to the changes. It is advisable to create a written amendment that outlines the modifications and have both parties sign it to ensure clarity and legal enforceability.

If a borrower defaults on a Promissory Note, the lender has several options. These may include:

It is important for borrowers to communicate with lenders if they are facing difficulties in making payments.

Florida Promissory Note templates can be found online through legal document preparation websites, local legal aid organizations, or by consulting with an attorney. Ensure that the template you choose complies with Florida state laws and suits your specific needs.