Legal Loan Agreement Document

Legal Loan Agreement Document

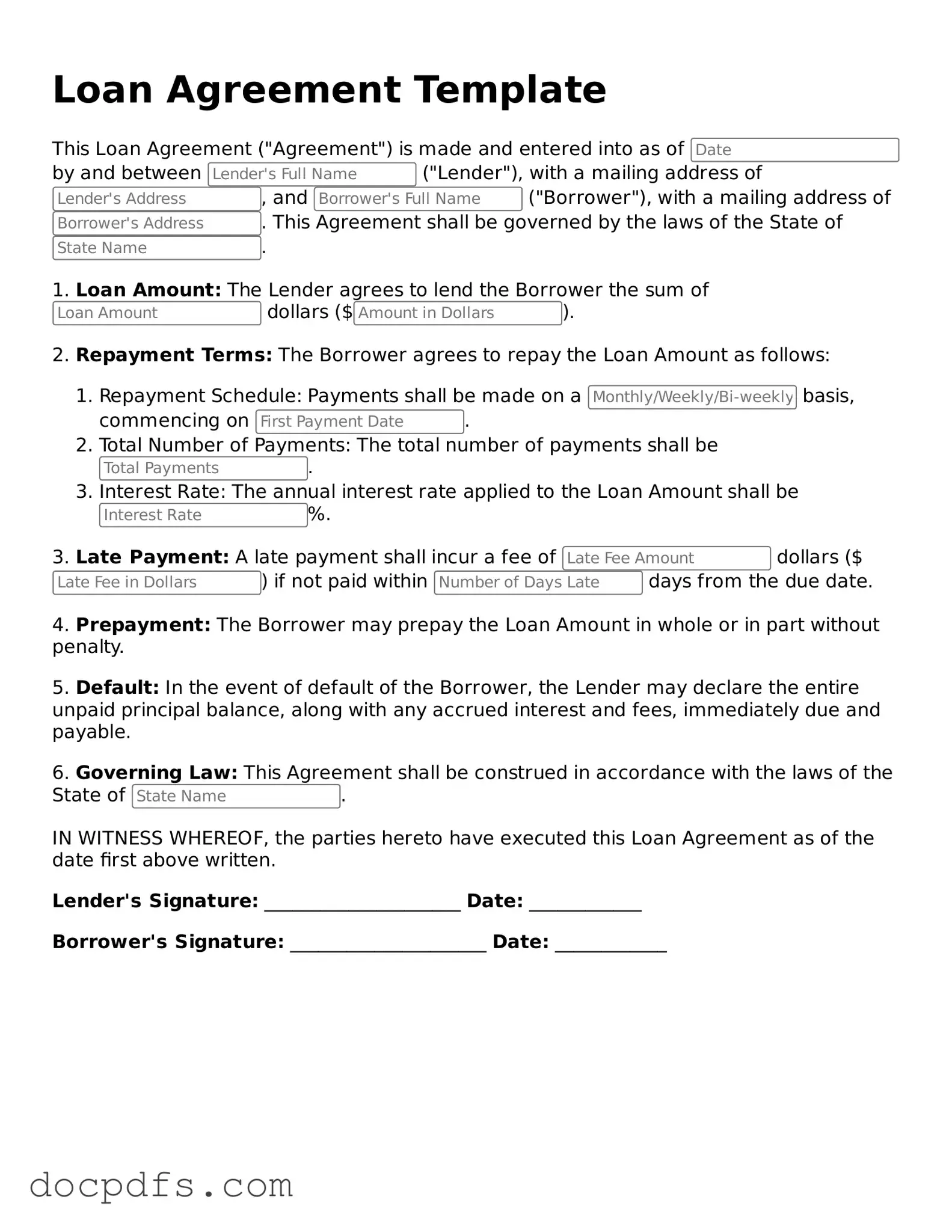

When individuals or businesses seek to borrow money, a Loan Agreement form serves as a crucial document that outlines the terms and conditions of the loan. This form typically includes essential details such as the principal amount being borrowed, the interest rate applicable, and the repayment schedule. Additionally, it specifies the duration of the loan, which can vary widely depending on the agreement between the lender and borrower. The agreement often includes clauses that address late payment penalties, collateral requirements, and the rights of both parties in case of default. By clearly articulating these terms, the Loan Agreement helps to protect the interests of both the lender and the borrower, ensuring that all parties understand their obligations and rights. Furthermore, it may also outline the governing law, which indicates the legal jurisdiction that will apply in case of disputes. Overall, a well-structured Loan Agreement form is essential for fostering trust and clarity in financial transactions.

How to Make a Pdf Invoice - Enhance your billing accuracy with straightforward invoice generation.

Understanding the importance of having a reliable legal mechanism in place is essential for everyone, and the Durable POA form in Maryland serves as a vital safeguard for your interests, ensuring that your designated agent can take necessary actions on your behalf when you cannot. Filling out this form is an important step towards securing your financial and health-related decisions according to your wishes, providing peace of mind for you and your loved ones.

I9 - The form typically includes dates of employment.

When entering into a Loan Agreement, several other forms and documents may be necessary to ensure clarity and legal protection for all parties involved. Below is a list of commonly used documents that complement a Loan Agreement.

Having these documents prepared and understood can help facilitate a smoother lending process. Always consult with a legal professional if you have questions or need assistance with these forms.

When filling out a Loan Agreement form, it's essential to approach the task with care. Here are some important dos and don'ts to keep in mind:

When filling out and using a Loan Agreement form, it is essential to keep several key points in mind. Below is a list of important takeaways that will help ensure a smooth process.

By following these guidelines, individuals can navigate the Loan Agreement process more effectively.

Filling out the Loan Agreement form is an important step in securing your loan. It is essential to provide accurate information to ensure a smooth process. Follow these steps carefully to complete the form correctly.

Once you have completed the form, make sure to keep a copy for your records. Submitting the form promptly will help you move forward with the loan process.

A Loan Agreement form is a legal document that outlines the terms and conditions of a loan between a lender and a borrower. It serves to protect both parties by clearly stating the amount borrowed, the interest rate, repayment schedule, and any other relevant terms. This document helps to prevent misunderstandings and provides a record of the agreement.

When drafting a Loan Agreement, it’s important to include several key elements to ensure clarity and enforceability. These elements typically include:

While it's not legally required to have a lawyer draft a Loan Agreement, consulting one can be beneficial. A legal professional can ensure that the agreement complies with state laws and adequately protects your interests. If the loan involves a significant amount of money or complex terms, professional guidance is especially advisable.

Yes, a Loan Agreement can be modified after it is signed, but both parties must agree to the changes. It’s essential to document any modifications in writing and have both parties sign the updated agreement. This helps maintain clarity and prevents future disputes regarding the terms of the loan.

If a borrower defaults on the Loan Agreement, the lender has several options, which may include:

It’s crucial for both parties to understand the consequences of defaulting and to communicate openly if financial difficulties arise.

While a verbal agreement can be legally binding in some cases, it is not recommended for loans. Without a written document, it can be challenging to prove the terms of the agreement in case of a dispute. A written Loan Agreement provides clear evidence of the terms and helps protect both the lender and borrower.