Legal Promissory Note for a Car Document

Legal Promissory Note for a Car Document

When purchasing a car through financing, understanding the Promissory Note for a Car form is essential for both buyers and sellers. This document serves as a written promise from the buyer to repay a specified amount of money to the lender, typically over a set period. It outlines key details such as the total loan amount, interest rate, payment schedule, and any applicable fees. In addition to these financial specifics, the form also includes information about the vehicle being financed, ensuring that both parties are clear on what is being purchased. Furthermore, the note often details the consequences of defaulting on payments, emphasizing the importance of adhering to the agreed-upon terms. By grasping the components and implications of this form, individuals can navigate the car financing process more effectively, fostering a smoother transaction and a clearer understanding of their financial obligations.

Release and Satisfaction of Promissory Note - This document officially releases the borrower from debt.

For those interested in securing financing, our guide on the essential features of a Promissory Note is invaluable. This form not only clarifies the obligations of both parties but also reinforces the legal binding nature of the agreement, providing peace of mind in your financial arrangements. For further details, visit our expert resources on Promissory Note templates.

When entering into a financing agreement for a vehicle, several documents often accompany the Promissory Note for a Car. Each of these documents serves a specific purpose and helps clarify the terms of the agreement. Below is a list of five commonly used forms that may be required or beneficial in conjunction with the Promissory Note.

In summary, these documents work together to ensure a clear and legally binding agreement between the parties involved in the vehicle purchase. Understanding each document's role can help facilitate a smoother transaction and provide peace of mind for both the buyer and seller.

When filling out a Promissory Note for a Car, it's important to be thorough and accurate. Here are some key do's and don'ts to keep in mind:

When filling out and using the Promissory Note for a Car form, consider the following key takeaways:

These takeaways can help ensure a smooth process when using the Promissory Note for a Car form.

Filling out a Promissory Note for a car is an important step in formalizing a loan agreement between the buyer and the seller. After completing this form, both parties will have a clear understanding of the terms and obligations involved. Below are the steps to guide you through the process of filling out the form accurately.

By following these steps, you will create a clear and enforceable agreement that protects both the borrower and the lender. Ensure that all information is accurate and that both parties understand their responsibilities before signing the document.

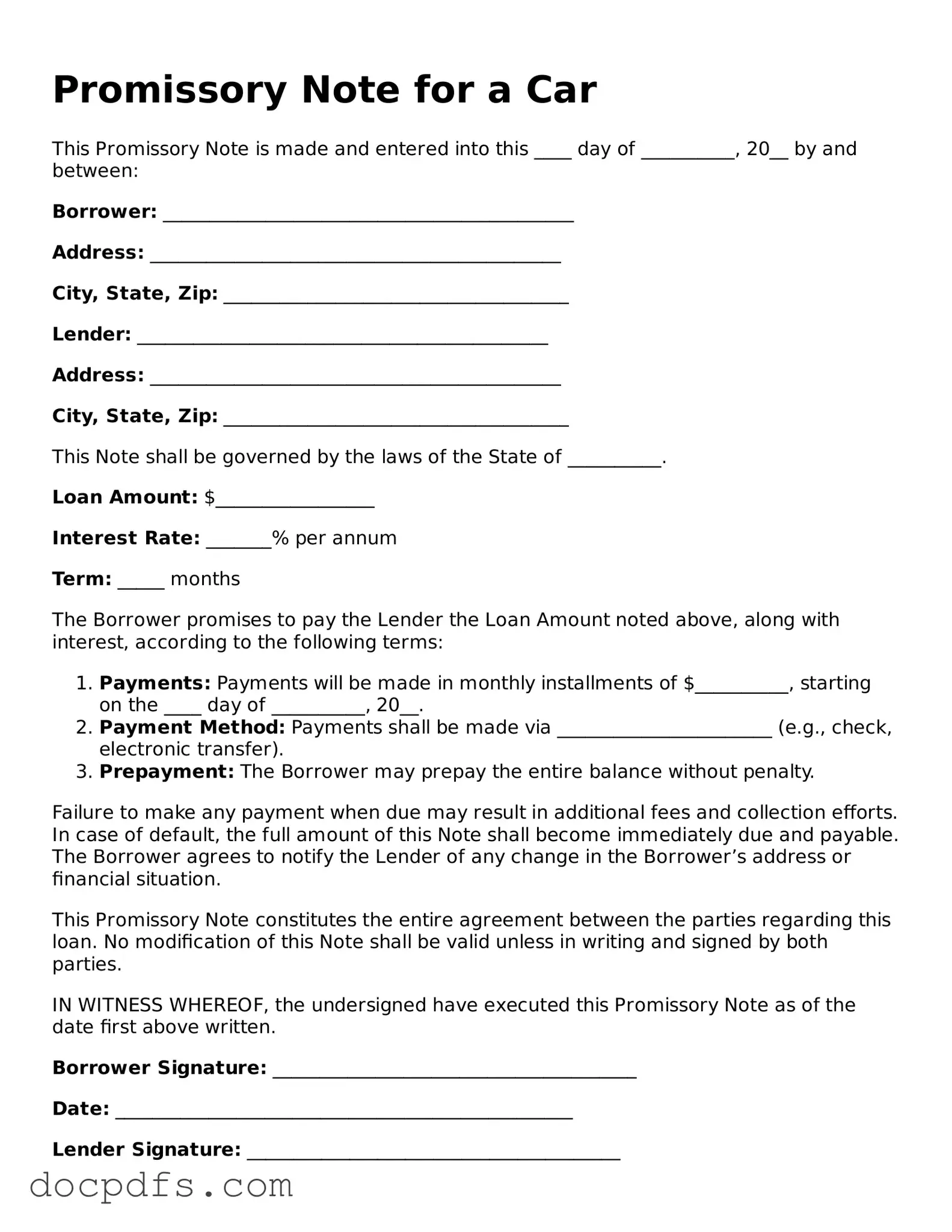

A Promissory Note for a Car is a legal document in which one party (the borrower) agrees to pay a specific amount of money to another party (the lender) under agreed-upon terms. This document outlines the details of the loan, including the amount borrowed, interest rate, repayment schedule, and any collateral involved, which in this case is the vehicle being financed.

A Promissory Note serves several important purposes:

When drafting a Promissory Note for a Car, it is essential to include the following information:

While both documents serve to outline the terms of a loan, they differ in complexity and detail. A Promissory Note is typically simpler and focuses primarily on the borrower's promise to repay the loan. In contrast, a loan agreement is more comprehensive, often including additional terms such as covenants, representations, and warranties. A loan agreement may also cover broader aspects of the lending relationship beyond just the repayment of the loan.

Yes, modifications can be made to a Promissory Note, but both parties must agree to the changes. It is important to document any amendments in writing and have both parties sign the revised note. This ensures that the modifications are legally binding and enforceable.

If a borrower defaults on the Promissory Note, the lender has several options. Typically, the lender can:

It is always best to communicate with the lender as soon as difficulties arise to avoid escalation.