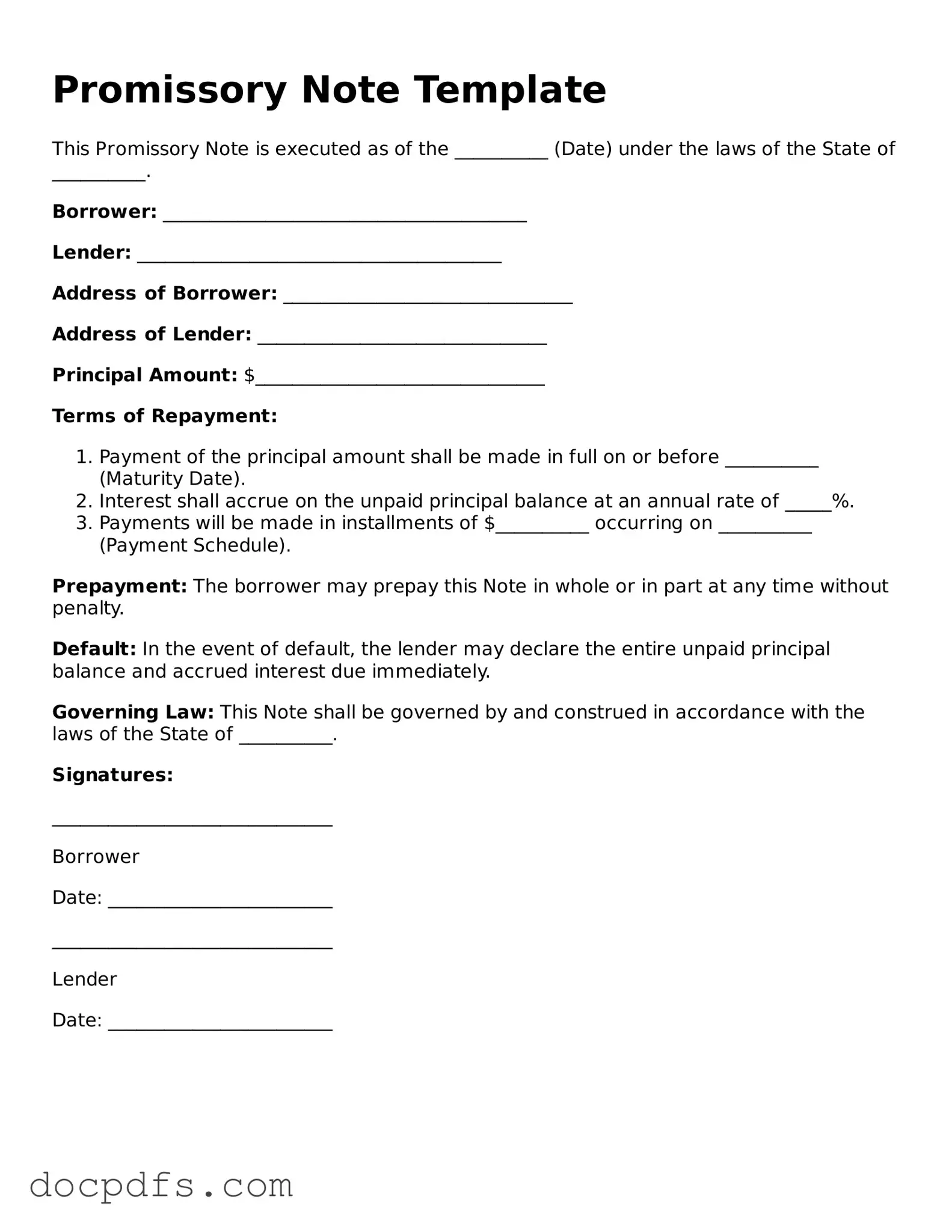

A Promissory Note is an essential financial document used in various lending transactions. This form serves as a written promise from one party, known as the borrower, to repay a specified sum of money to another party, referred to as the lender, under agreed-upon terms. Key elements typically included in a Promissory Note are the principal amount, the interest rate, and the repayment schedule, which outlines when payments are due. Additionally, the document may detail the consequences of default, providing clarity on what happens if the borrower fails to meet their obligations. Signatures from both parties are crucial, as they signify agreement and commitment to the terms laid out in the note. Understanding the nuances of this form can help both lenders and borrowers navigate their financial agreements more effectively, ensuring that expectations are clear and legally enforceable.

Lease Non Renewal Notice - Landlords may use this form to avoid automatic lease extensions with tenants.

Living Will Downloadable 5 Wishes Printable Version - Five Wishes allows you to communicate what brings you comfort during challenging health situations.

A New York Hold Harmless Agreement is a legal document designed to protect one party from liability or claims arising from another party's actions or negligence. This agreement ensures that if an incident occurs, the party signing the form agrees to take responsibility and indemnify the other party. For those seeking further information, New York PDF Docs provides an excellent resource. Understanding this form is crucial for individuals and businesses looking to mitigate risk in various activities and transactions.

Vehicle Sale Agreement Format in Word - Ensures compliance with state laws regarding vehicle sales.

A Promissory Note is a crucial document in lending transactions, but it often works in conjunction with several other forms and documents. Understanding these related documents is essential for both lenders and borrowers to ensure clarity and legal compliance in financial agreements.

In summary, these documents work together to create a clear framework for the lending process. Each plays a vital role in protecting the interests of both lenders and borrowers. Familiarity with these forms can help avoid misunderstandings and potential legal issues down the line.

When filling out a Promissory Note form, it's essential to be thorough and accurate. Here are some important do's and don'ts to keep in mind:

When filling out and using a Promissory Note form, consider the following key takeaways:

Once you have the Promissory Note form in hand, the next steps involve carefully filling it out to ensure all necessary details are included. This document will require specific information related to the loan agreement, and accuracy is crucial. Follow the steps outlined below to complete the form correctly.

After completing these steps, review the form for any errors or omissions. It's advisable to keep a copy for your records. Once everything is in order, the form can be executed, and the loan can proceed according to the terms laid out in the document.

A Promissory Note is a written promise to pay a specified amount of money to a designated person or entity at a certain time or on demand. It outlines the terms of the loan, including interest rates and payment schedules.

Individuals and businesses often use Promissory Notes. They are commonly utilized in personal loans, business financing, and real estate transactions. Both lenders and borrowers benefit from the clarity and structure that a Promissory Note provides.

A typical Promissory Note includes the following elements:

While both documents serve to outline the terms of a loan, a Promissory Note is generally simpler and focuses solely on the promise to pay. A loan agreement, on the other hand, may include additional terms, conditions, and responsibilities for both parties involved.

Yes, a properly executed Promissory Note is legally binding. It creates an obligation for the borrower to repay the loan according to the agreed-upon terms. However, enforceability may depend on local laws and the clarity of the document.

Yes, a Promissory Note can be modified if both parties agree to the changes. It’s important to document any modifications in writing to avoid misunderstandings in the future.

If the borrower defaults, the lender may take legal action to recover the owed amount. This could involve filing a lawsuit or pursuing collection efforts. Having a clear Promissory Note can help facilitate this process.

While it's not required to have a lawyer draft a Promissory Note, consulting one can be beneficial, especially for larger loans or complex agreements. A legal expert can ensure that the document meets all necessary legal standards.

Templates for Promissory Notes are widely available online. Many legal websites offer free or paid templates that you can customize to fit your specific needs. Always ensure that the template complies with your state’s laws.